Every business owner should know exactly how many units they need to sell — or how much revenue they need to generate — before they start making a profit. That number is your break-even point, and break even analysis is the tool that reveals it. Whether you are launching a new product, adjusting pricing, or deciding whether to hire, break even analysis gives you the hard numbers behind the decision.

Table of Contents

- Key Takeaways

- What Is Break-Even Analysis?

- The Break-Even Formula Explained

- How to Calculate Your Break-Even Point

- 5 Ways to Use Break-Even Analysis in Your Business

- Common Mistakes That Skew Your Numbers

- Beyond the Basics: Margin of Safety and Sensitivity Analysis

- Break-Even Analysis Checklist

- Frequently Asked Questions

Key Takeaways

| Area | Key Insight |

|---|---|

| What it tells you | The exact revenue or unit volume where your business stops losing money |

| Core formula | Fixed Costs ÷ (Price per Unit − Variable Cost per Unit) |

| When to use | Pricing decisions, new product launches, cost restructuring, hiring |

| How often | Recalculate whenever costs, pricing, or product mix changes |

| Biggest pitfall | Miscategorizing costs as fixed vs. variable |

What Is Break-Even Analysis?

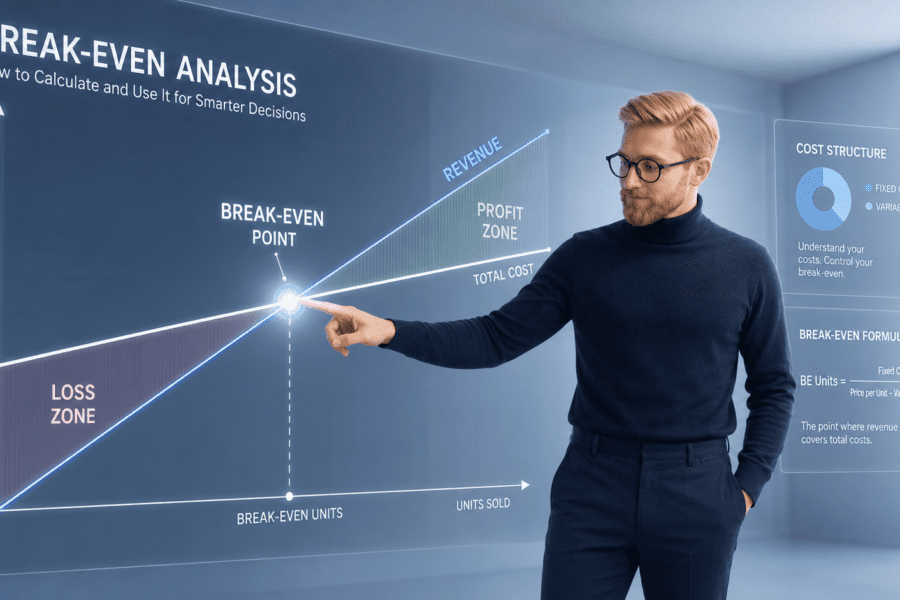

Break even analysis is a financial calculation that determines the point at which total revenue equals total costs — meaning your business generates neither profit nor loss. Everything above the break-even point is profit; everything below is a loss.

For SMB owners generating $500K to $20M in revenue, this is not just a textbook exercise. It is a practical decision-making tool that answers critical questions: Can I afford to lower my price to win a contract? What happens to profitability if my rent increases 20%? How many clients do I need before this new service line pays for itself?

Why it matters more than you think

Most business owners have a rough intuition about profitability, but intuition fails when conditions change. A 10% cost increase and a 5% price cut might seem manageable individually, but combined they could push your break-even point up by 40%. Without running the numbers, you would never see that coming. As we covered in our guide on unit economics, understanding the math behind each unit of your business is the foundation of smart financial decisions.

The Break-Even Formula Explained

The basic formula

Break-Even Point (units) = Fixed Costs ÷ (Selling Price per Unit − Variable Cost per Unit)

The denominator — selling price minus variable cost — is called the contribution margin. It represents how much each unit sold contributes toward covering fixed costs and eventually generating profit.

Revenue-based formula

If your business does not sell discrete units (like a consulting firm), use the revenue version:

Break-Even Revenue = Fixed Costs ÷ Contribution Margin Ratio

Where Contribution Margin Ratio = (Revenue − Variable Costs) ÷ Revenue

Understanding cost categories

| Cost Type | Definition | Examples |

|---|---|---|

| Fixed costs | Stay the same regardless of sales volume | Rent, salaries, insurance, loan payments, software subscriptions |

| Variable costs | Change in direct proportion to sales volume | Materials, shipping, sales commissions, payment processing fees |

| Semi-variable | Have both fixed and variable components | Utilities, some labor costs, phone plans with overage charges |

Getting this classification right is critical. If you misclassify a variable cost as fixed, your break-even calculation will be wrong — and you will make decisions based on faulty numbers. For a deeper look at how to categorize costs correctly, see our guide on financial management for SMEs.

How to Calculate Your Break-Even Point: Step by Step

Step 1: List all fixed costs

Add up every cost that does not change with sales volume over your analysis period (typically monthly). Include rent, salaried employees, insurance, software, loan payments, and any other overhead. For most SMBs in the $1-10M range, monthly fixed costs fall between $30,000 and $200,000.

Step 2: Determine variable cost per unit

Calculate how much it costs to produce or deliver one additional unit of your product or service. For a product business, this includes materials, direct labor, packaging, and shipping. For a service business, it might be contractor hours, travel costs, or per-project software licenses.

Step 3: Set your selling price per unit

Use your actual average selling price, not list price. Account for discounts, volume pricing, and any concessions you regularly make. If you need help with pricing strategy, our pricing strategy guide covers this in depth.

Step 4: Calculate contribution margin

Contribution Margin = Selling Price − Variable Cost

Example: If you sell a product for $150 and variable costs are $60, your contribution margin is $90. Each unit sold puts $90 toward covering fixed costs.

Step 5: Divide fixed costs by contribution margin

If your monthly fixed costs are $45,000 and contribution margin is $90 per unit:

Break-Even = $45,000 ÷ $90 = 500 units per month

You need to sell 500 units monthly to cover all costs. Unit 501 is where profit begins.

Worked example: service business

A marketing agency has monthly fixed costs of $80,000 (salaries, office, tools). Average project revenue is $12,000 with $4,800 in variable costs (freelancers, ad spend pass-through).

- Contribution margin per project: $12,000 − $4,800 = $7,200

- Break-even: $80,000 ÷ $7,200 = 11.1 projects per month

- The agency needs to complete at least 12 projects monthly to be profitable

5 Ways to Use Break-Even Analysis in Your Business

1. Pricing decisions

Before changing your price, run a break-even analysis at the new price point. A 10% price drop might seem small, but it could increase your break-even volume by 30% or more. Ask yourself: can I realistically generate that much additional volume?

2. New product or service launches

Before investing in a new offering, calculate its break-even point separately. How many months will it take to reach break-even? Is the required volume realistic given your market size and sales capacity? This prevents launching products that sound exciting but never pay for themselves.

3. Cost restructuring

When considering a major cost change — new hire, office move, equipment purchase — recalculate your break-even point. A $5,000/month salary increase raises your break-even by $5,000 ÷ contribution margin in additional units needed. That makes the decision concrete.

4. Investor and lender conversations

Banks and investors want to know your break-even point. It demonstrates financial literacy and helps them assess risk. A business operating well above its break-even has a safety cushion; one hovering near break-even is fragile. For more on preparing financials for outside capital, see how to attract financing for your business.

5. Scenario planning

Run “what if” scenarios: What if materials costs rise 15%? What if you lose your biggest client? What if you add a second shift? Break even analysis turns anxiety into arithmetic. You stop guessing and start knowing exactly how much buffer you have.

Common Mistakes That Skew Your Numbers

1. Mixing up fixed and variable costs

Salaries are fixed if you pay them regardless of output. But sales commissions are variable. Rent is fixed — but overtime labor is variable. Misclassifying even one major cost item can throw off your entire analysis by 20-30%.

2. Ignoring semi-variable costs

Some costs are both: a warehouse team might be fixed at baseline but require overtime (variable) during peak periods. Split these into their fixed and variable components for accuracy.

3. Using outdated numbers

If you calculated break-even six months ago with old cost data, it is no longer reliable. Supplier prices change, employee costs shift, and market conditions evolve. Recalculate quarterly at minimum.

4. Forgetting about product mix

If you sell multiple products at different margins, a simple single-product break-even formula does not work. You need a weighted average contribution margin that reflects your actual sales mix. When the mix shifts toward lower-margin products, your break-even point rises — even if total volume stays constant.

5. Assuming linear relationships

The basic formula assumes that variable costs per unit and selling prices stay constant. In reality, you may get volume discounts on materials (lowering variable costs) or need to discount prices to sell more (lowering revenue per unit). Account for these step changes in your analysis.

Beyond the Basics: Margin of Safety and Sensitivity Analysis

Margin of safety

Your margin of safety is the gap between current sales and the break-even point, expressed as a percentage:

Margin of Safety = (Current Sales − Break-Even Sales) ÷ Current Sales × 100%

A 25% margin of safety means sales could drop 25% before you start losing money. Most healthy businesses target a margin of safety of 20-30%. Below 15% is a warning sign — you are one bad quarter away from losses.

Sensitivity analysis

Run your break even analysis at multiple price points and cost levels. Build a simple table:

| Scenario | Fixed Costs | Price | Variable Cost | Break-Even Units |

|---|---|---|---|---|

| Base case | $45,000 | $150 | $60 | 500 |

| Price cut 10% | $45,000 | $135 | $60 | 600 |

| Cost increase 15% | $45,000 | $150 | $69 | 556 |

| Both combined | $45,000 | $135 | $69 | 682 |

This table shows that a modest price cut combined with a cost increase raises break-even by 36% — from 500 to 682 units. That is the kind of insight that prevents bad decisions.

For a broader view of how to stress-test your financial assumptions, read our article on financial KPIs every business owner should track.

Break-Even Analysis Checklist

- ☐ List all monthly fixed costs (rent, salaries, insurance, subscriptions)

- ☐ Calculate variable cost per unit or per project

- ☐ Determine actual average selling price (after discounts)

- ☐ Compute contribution margin (price minus variable cost)

- ☐ Calculate break-even in units: Fixed Costs ÷ Contribution Margin

- ☐ Calculate break-even in revenue: Fixed Costs ÷ CM Ratio

- ☐ Calculate your margin of safety percentage

- ☐ Run sensitivity analysis with 3-5 scenarios

- ☐ Compare break-even volume to your realistic sales capacity

- ☐ Set a calendar reminder to recalculate quarterly

Want help calculating your break-even point and using it to drive smarter decisions? Our team works with SMB owners every day to turn financial data into actionable strategy. Book a free consultation and let us run the numbers together.

Frequently Asked Questions

What is a good break-even point for a small business?

There is no universal answer — it depends on your industry, business model, and growth stage. What matters is how your break-even compares to your realistic sales capacity. If you can comfortably sell 2x your break-even volume, you have a healthy buffer. If you are barely hitting break-even most months, your business model needs restructuring — either raise prices, cut costs, or both.

How often should I recalculate my break-even point?

At minimum, quarterly. But recalculate immediately whenever a major input changes: new pricing, significant cost changes, losing or gaining a major client, or entering a new market. The businesses that use break even analysis as an ongoing tool — not a one-time exercise — make consistently better decisions.

Can break-even analysis work for service businesses?

Absolutely. Instead of “units,” think in terms of projects, clients, or billable hours. A consulting firm with $60,000 in monthly fixed costs and an average contribution margin of $5,000 per engagement needs 12 engagements to break even. The formula is identical — only the definition of a “unit” changes.

What is the difference between break-even analysis and profitability analysis?

Break even analysis tells you the minimum threshold — where losses stop. Profitability analysis goes further, examining how much profit you make at various sales levels and which products or services contribute most. Think of break-even as the floor and profitability analysis as the map of the entire building above it.

Should I include owner salary in fixed costs?

Yes, always. If you are not paying yourself a market-rate salary, your break-even calculation is artificially low and your “profit” is really just unpaid wages. Include a reasonable owner compensation in fixed costs to get an honest picture of whether the business is truly viable.