Financial Scenario Planning Benchmarks

| Metric | Benchmark |

|---|---|

| Standard scenario set | Base, downside (-20%), upside (+20%) |

| Stress test for customer concentration | Loss of top 1-3 customers |

| Stress test for AR slowdown | DSO +30 days for 90 days |

| Refresh frequency (scenarios) | Quarterly minimum |

| Time to build first scenario model | 2-4 weeks |

| SMBs that model downside scenarios | ~30% (NFIB survey) |

| Cost of scenario planning (DIY in Excel) | 20-40 hours initial build |

| Cash reserve target (worst-case scenario) | 3+ months opex after stress test |

Most business owners assume that a solid financial forecast is enough to navigate uncertainty. It isn’t. A single forecast tells you one story about the future, but the future rarely follows a script. SMEs using scenario planning show measurably higher resilience and growth rates compared to those relying on forecasts alone. This guide will show you exactly what financial scenario planning is, why it’s different from forecasting and budgeting, and how you can use it right now to make smarter, faster decisions for your business.

Table of Contents

- What is financial scenario planning?

- Scenario planning vs. forecasting and budgeting

- Why scenario planning matters for small and medium businesses

- How to conduct effective financial scenario planning

- A CFO’s perspective: What most scenario planning guides miss

- Get expert help with your scenario planning

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| More than forecasting | Financial scenario planning explores multiple futures, giving SMBs an edge over relying on single forecasts. |

| Boosts resilience | Businesses with scenario planning adapt faster and perform better during market volatility. |

| Three focused scenarios | Stick to best, base, and worst case scenarios for clear, actionable decision-making. |

| Triggers drive decisions | Link plans to specific events (like a sales drop) so you know exactly when to act. |

| Ongoing updates required | Keep your scenarios fresh by revisiting them every quarter or after major changes. |

What is financial scenario planning?

Financial scenario planning means building financial models for at least three different versions of your future. Not one future. Three. You map out what happens if things go well, what happens if they go sideways, and what happens if they go badly. Then you decide in advance what you’d do in each case.

This is fundamentally different from financial planning basics, which typically involves setting goals and creating a single path to reach them. Scenario planning accepts uncertainty as a given and prepares you to respond to it, rather than being blindsided by it.

Here’s what makes scenario planning so powerful for small and medium businesses: it forces you to think through your assumptions before they’re tested by reality. When a supply chain disruption hits, or a key client walks away, you aren’t scrambling to figure out what to do. You already have a plan.

“Scenario planning explores multiple hypothetical futures, unlike forecasting which predicts one likely outcome.” — ICAEW Financial Modelling Guidance

Forecasting says: “Based on current trends, we expect $500,000 in revenue next quarter.” Scenario planning says: “If revenue hits $500,000, here’s our plan. If it drops to $350,000, here’s what we cut. If it jumps to $700,000, here’s how we scale.”

Scenario planning is also distinct from custom modeling for business, which is the technical tool you use to build the models themselves. Think of scenario planning as the strategy and financial modeling as the execution.

Here’s what good scenario planning helps you do:

- Answer ‘what if’ questions before they become real problems (e.g., What if our top client cancels?)

- Stress-test your business model under different economic conditions

- Align your leadership team on agreed responses before a crisis hits

- Identify the early warning signs that tell you which scenario is actually unfolding

- Plan for growth opportunities with confidence (e.g., What if we expand to a new market?)

- Protect cash flow by mapping how different outcomes affect your bank balance

This isn’t a tool reserved for Fortune 500 strategy departments. It’s one of the highest-leverage things a small business owner can do.

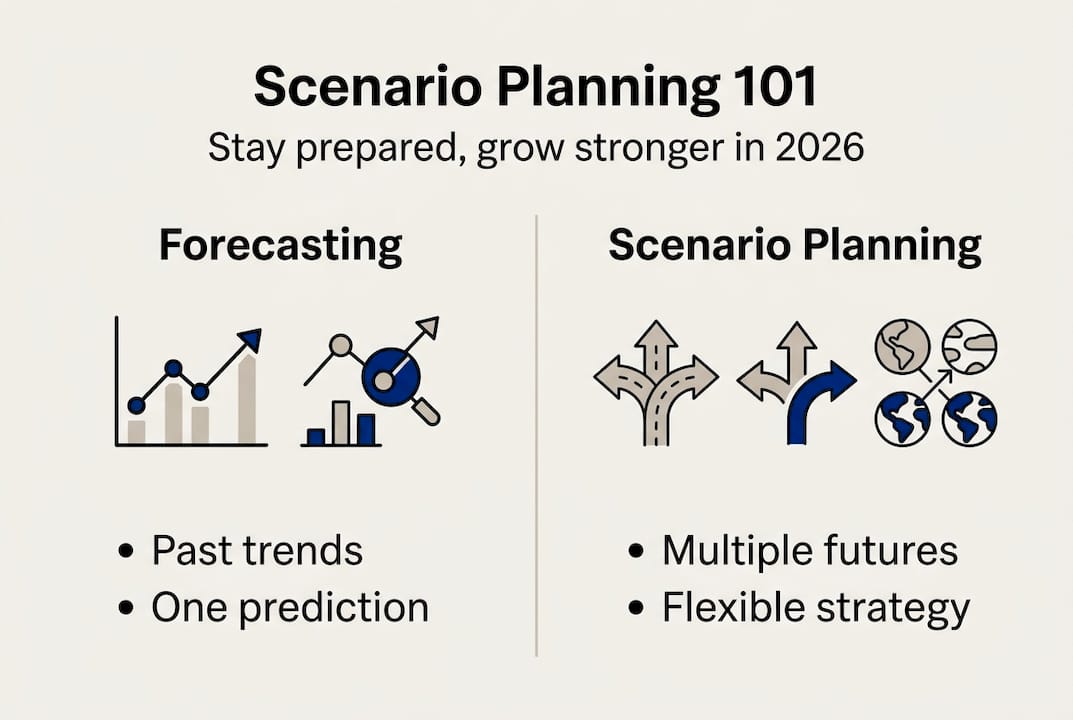

Scenario planning vs. forecasting and budgeting

Once you know what scenario planning is, the next step is understanding how it works alongside your other financial tools. Most business owners use forecasting and budgeting regularly. Scenario planning doesn’t replace them. It makes them far more useful.

| Tool | Primary purpose | Time horizon | Flexibility | Business use case |

|---|---|---|---|---|

| Scenario planning | Explore multiple futures | Long-term (1-5 years) | High | Strategic decisions, risk planning |

| Forecasting | Predict one likely outcome | Short to medium-term | Medium | Operational planning, investor reporting |

| Budgeting | Set fixed financial targets | Annual | Low | Expense control, performance tracking |

Scenario planning is strategic. Forecasting is operational. Budgeting is about control. Each one answers a different question. Scenario planning asks “what could happen?” Forecasting asks “what will probably happen?” Budgeting asks “what are we allowed to spend?”

A real-world example makes this clear. Tetra Pak, the packaging giant, famously reduced its planning cycles and improved decision speed by integrating scenario planning alongside its standard forecasting processes. The key insight was that scenario planning complements forecasting and budgeting rather than replacing them. Businesses that use all three tools together respond faster to market shifts and make more confident investment calls.

For SMBs, the practical implication is simple. Your budget tells you where your money is going. Your forecast tells you where the business is headed. Your scenarios tell you what to do if the heading changes.

Pro Tip: Never rely on only one of these tools in isolation. A budget without scenarios is a fixed target in a moving market. Scenarios without a forecast give you no operational baseline. Use all three, and they will reinforce each other.

If you’re still unclear on how forecasting and budgeting interact, the breakdown in budgeting vs forecasting is a practical starting point before layering in scenario planning.

Why scenario planning matters for small and medium businesses

Here’s a number that should get your attention. SMB average monthly earnings were $83,600 in October 2025, down 21% month over month. A 21% revenue swing in a single month. For a business with tight margins and a lean team, that’s not a dip. That’s a crisis, unless you planned for it.

| Planning approach | Response to 20% revenue drop | Typical outcome |

|---|---|---|

| No formal planning | Reactive scrambling, delayed decisions | Cash shortfall, missed payroll |

| Forecast only | Recognized the gap, no pre-built response | Slow to act, partial recovery |

| Scenario planning adopted | Activated pre-planned cost controls | Stabilized within 30-60 days |

The table above reflects a pattern we see repeatedly. The businesses that survive sudden market shifts aren’t always the biggest or the most well-funded. They’re the ones that thought through the “what ifs” before those scenarios became real.

Following proven steps for SME profitability matters, but scenario planning gives those steps a safety net. It answers what you do when your profitability strategy encounters an unexpected roadblock.

Here are four real-world risks that scenario planning directly addresses for SMBs:

- Supply chain disruption: A key supplier raises prices by 30% or goes under entirely. Your scenario plan already maps out your backup suppliers and the margin impact.

- Market demand shift: Customer demand drops fast because of economic pressure or a competitor entering your market. Your downside scenario tells you exactly what costs to trim and when.

- Cash crunch: Revenue is fine but timing is off. Invoices come in late and bills come in early. SMB risk mitigation through scenario planning flags these timing risks before they become emergencies.

- Expansion risk: You’re considering hiring, opening a new location, or entering a new market. Scenario planning stress-tests the investment across multiple demand levels so you know your break-even point.

Scenario planning doesn’t eliminate risk. It ensures that risk never catches you completely off guard.

How to conduct effective financial scenario planning

Knowing why scenario planning matters is one thing. Doing it well is another. Here’s a practical process you can apply to your own business, regardless of your size or industry.

Step-by-step process:

- Define your planning goals. What decisions are you trying to support? Hiring? Expansion? Surviving a slow quarter? Your scenarios should connect directly to the decisions you’re actually facing.

- Select three scenarios. Build a base case (most likely outcome), a best case (things go well), and a worst case (things go badly). Expert guidance consistently recommends limiting to three. More than three and the exercise becomes unmanageable.

- Build your financial models. Map out revenue, costs, cash flow, and margins under each scenario. Use your actual business numbers as the foundation. This is where a cash flow forecasting tool becomes essential.

- Assign decision triggers. For each scenario, define the specific indicator that tells you it’s unfolding. Example: if monthly revenue falls 10% below baseline for two consecutive months, activate cost reduction plan B.

- Review and update regularly. Set a calendar reminder. At minimum, revisit your scenarios every quarter and after any major market event.

Common pitfalls to avoid:

- Building too many scenarios and losing focus on any single one

- Treating the base case as guaranteed and ignoring the other two

- Forgetting to model cash flow timing, not just revenue and profit

- Building scenarios once and never updating them as your business changes

- Keeping scenarios confined to the finance team instead of sharing them with your leadership group

Pro Tip: Make each scenario a narrative, not just a spreadsheet. Write two or three sentences describing what’s happening in the market and in your business under each scenario. This makes the model far more actionable when you’re under pressure and need to act fast. A financial health checkup is a smart first step before you build your scenarios, so you’re starting with accurate baseline data.

A CFO’s perspective: What most scenario planning guides miss

Most guides treat scenario planning as a modeling exercise. Build three spreadsheets, label them best, base, and worst, and you’re done. That misses the point entirely.

The biggest reason scenario planning fails in small businesses isn’t a lack of data or a bad model. It’s that the scenarios get built once and never touched again. They become a document in a folder, not a living tool that shapes how you run your business week to week.

What actually works is treating scenario planning as an ongoing conversation with your numbers. The best business owners we work with revisit their scenarios whenever something shifts, a key contract, a market signal, a hiring decision. They involve their leadership teams so that everyone understands the triggers and the agreed responses. There are no surprises when the plan needs to activate.

Another thing most guides skip: the psychological component. When you’ve already decided what to do if revenue drops 15%, you can make that call fast and without panic. That speed is worth more than any spreadsheet sophistication.

If your scenarios feel disconnected from how you actually run the business, it may be time to look at the signs your business needs a CFO for outside perspective. A fractional CFO can help you build scenarios that are genuinely actionable, not just theoretically complete.

Get expert help with your scenario planning

Scenario planning delivers real results when it’s built on solid data and updated consistently. For many SMB owners, the challenge isn’t understanding the concept. It’s finding the time and expertise to do it well.

At John Galt Finance, we help small and medium businesses build custom scenario models grounded in their actual financials. Whether you need a one-time model or ongoing CFO support, we bring the strategic depth that makes planning actionable. Start with our business planning guide to build a strong foundation, use the cash flow toolkit to sharpen your cash projections, and explore our custom modeling process to see how we tailor models to your business. Reach out for a consultation and turn your scenario planning from a spreadsheet into a strategic advantage.

Frequently asked questions

What are the three main scenarios I should plan for?

Plan for a best case, base case, and worst case scenario. Sticking to three keeps the process manageable and ensures each scenario gets the attention it deserves.

How often should I update my financial scenarios?

Review your scenarios at least quarterly and after any significant business or market event. Not updating scenarios is one of the most common and costly mistakes SMB owners make.

Is financial scenario planning only for large companies?

Not at all. SMEs using scenario planning consistently show higher resilience and better growth outcomes, making it one of the highest-value practices for small and medium businesses.

How does scenario planning relate to cash flow?

Each scenario you model will show a different cash flow outcome, revealing potential shortfalls before they arrive. Ignoring cash flow in your scenarios is a critical mistake that leaves you vulnerable to timing crunches even when revenue looks healthy.

Recommended

- Essential financial metrics to track for SMB growth: 2026

- Unlock business growth with a custom financial modeling process

- Cash Flow Forecasting: How to Never Run Out of Money | John Galt

- Financial Planning for Business Owners: A Practical Guide | John Galt

FAQ

What scenarios should I always model?

Five essentials: (1) base case (most likely), (2) downside (-20% revenue), (3) upside (+20% revenue), (4) loss of largest customer, (5) AR slowdown of 30 days for 90 days. Together they capture the main risks any SMB faces.

How is scenario planning different from forecasting?

Forecasting is your best estimate of the future. Scenario planning is multiple plausible futures with action plans for each. Forecasting answers “what will happen?”; scenarios answer “what will we do if X happens?”. Mature finance functions do both.

How often should I refresh scenarios?

Quarterly at minimum, plus any time you have a major external shock (recession warning, supply chain disruption, regulatory change). Outdated scenarios can be worse than no scenarios; they create false confidence.

What’s the right tool for scenario planning?

For SMBs under $10M revenue, Excel with scenario manager is sufficient. Between $10M-$50M, tools like Jirav, Vena, or Cube speed up iteration and reduce error. Avoid enterprise tools (Anaplan, Hyperion) until $50M+; the setup cost exceeds the value.

How do I get my team to actually act on scenarios?

Tie each scenario to specific triggers and actions. Example: “If two consecutive months are 10% below plan, freeze hiring and cut marketing 30%.” Pre-committed decisions get executed; abstract scenarios get filed and forgotten.