Most e-commerce founders celebrate when revenue grows — but ecommerce financial planning reveals a harder truth: more sales don’t automatically mean more profit. Without a structured financial framework, growing online stores routinely face cash shortfalls, inventory crises, and margin erosion that no amount of top-line growth can fix.

This guide walks you through a complete ecommerce financial planning system — from understanding your true unit economics to building cash flow models that survive peak seasons and supply chain disruptions.

Table of Contents

- Why E-commerce Finance Is Different

- Unit Economics: The Foundation of Profitable Growth

- Cash Flow Management for Online Stores

- COGS and Margin Structure

- Essential Financial KPIs for E-commerce

- Budgeting and Forecasting for Seasonal Businesses

- Scaling Profitably: When Growth Destroys Value

- E-commerce Financial Planning Checklist

- FAQ

Key Takeaways

| Topic | What You Need to Know |

|---|---|

| Unit Economics | Calculate CAC, LTV, and contribution margin before scaling ad spend |

| Cash Flow | Inventory purchases and ad platforms create 30–60 day cash gaps |

| Gross Margin | Healthy e-commerce gross margins run 40–60%; below 30% is danger territory |

| Forecasting | Model 3 scenarios (base, upside, downside) for every peak season |

| CAC Payback | Aim for CAC payback under 6 months to preserve working capital |

Why E-commerce Finance Is Different

Traditional retail finance models don’t map cleanly onto online stores. E-commerce businesses face a unique combination of challenges:

- Inventory risk: You pay for goods weeks or months before you sell them, creating working capital strain.

- Platform dependency: Ad costs on Meta and Google fluctuate daily, making CAC volatile and hard to forecast.

- Returns complexity: Return rates of 15–30% are normal in e-commerce — and every return has hidden costs (restocking, shipping, damage write-offs).

- Marketplace fees: Amazon, Etsy, and Shopify all take a cut that reduces your effective margin.

- Seasonality concentration: Many e-commerce stores earn 30–50% of annual revenue in Q4 alone.

Effective ecommerce financial planning accounts for all of these dynamics — not just revenue and expenses.

Unit Economics: The Foundation of Profitable Growth

Before you scale anything, you need to understand your unit economics. These are the per-order and per-customer numbers that determine whether your business model is fundamentally sound.

Customer Acquisition Cost (CAC)

CAC = Total Marketing & Sales Spend ÷ Number of New Customers Acquired

Example: If you spend $20,000 on ads in March and acquire 400 new customers, your CAC is $50. The question is whether that $50 is justified by what each customer is worth to you over time.

Customer Lifetime Value (LTV)

LTV = Average Order Value × Purchase Frequency × Customer Lifespan × Gross Margin %

Example: A customer who buys twice per year at $80 average order value, stays for 2 years, and generates 45% gross margin has an LTV of $80 × 2 × 2 × 0.45 = $144.

LTV:CAC Ratio

| Ratio | Interpretation |

|---|---|

| Below 1:1 | You’re losing money on every customer — stop scaling |

| 1:1 to 2:1 | Marginal — only viable with very fast payback periods |

| 3:1 | Healthy — standard benchmark for funded e-commerce brands |

| 4:1+ | Strong — you have room to invest aggressively in growth |

Contribution Margin per Order

Contribution margin = Revenue − Variable Costs (COGS + shipping + payment processing + returns)

This is the most important number in ecommerce financial planning. It tells you exactly how much each order contributes to covering your fixed costs. A business with $500K in revenue but negative contribution margin is running a machine that destroys cash with every transaction.

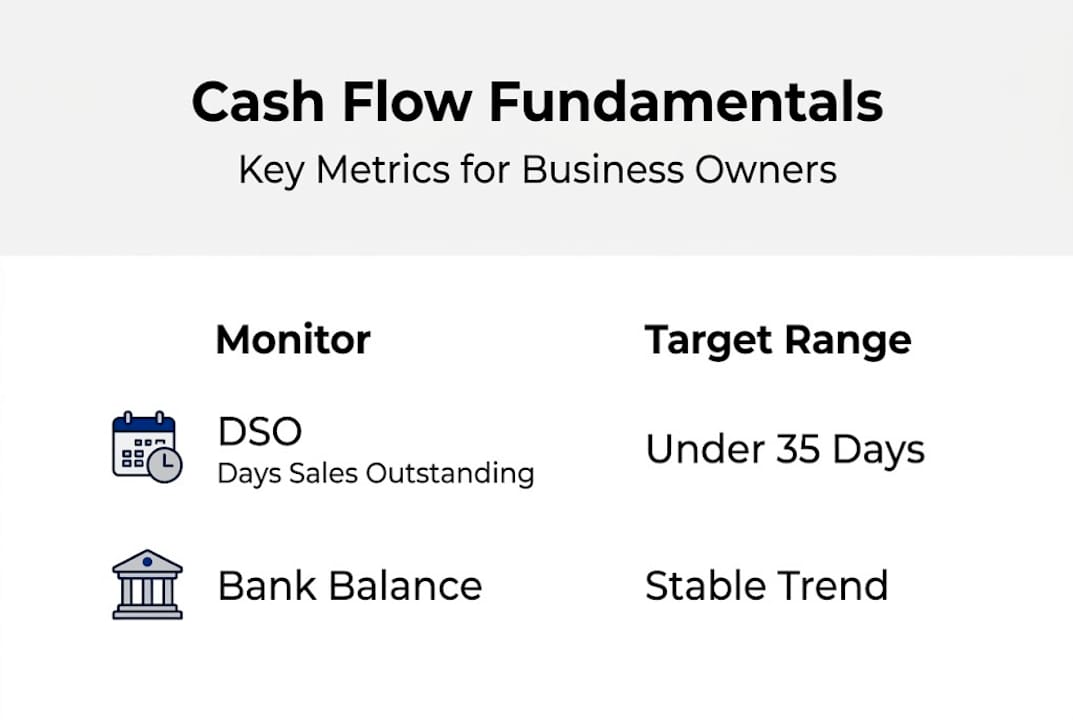

Cash Flow Management for Online Stores

Cash flow is where most e-commerce businesses hit the wall — not because they’re unprofitable, but because they’re growing. A scaling store needs to buy more inventory before it collects revenue from past sales. This creates a structural cash gap that surprises founders every time.

The Inventory Cash Gap

Here’s a typical scenario:

- Day 0: Place inventory order, pay supplier (or put deposit down) — cash out

- Day 30–45: Inventory arrives at warehouse

- Day 45–75: Products sell and ship to customers

- Day 75–90 (if marketplace): Platform pays out, cash in

That’s a 60–90 day cash cycle. Double your sales, and you double the cash you need to fund this cycle. See our full guide on how to improve cash flow for business owners for tactics to compress this gap.

13-Week Rolling Cash Flow Forecast

Every e-commerce operator should maintain a 13-week rolling cash forecast. This model tracks:

- Expected revenue collections (net of returns)

- Inventory purchase commitments

- Ad spend obligations

- Fixed operating expenses

- Debt service (if applicable)

The output is a week-by-week cash balance that shows you exactly when you’ll hit a shortfall — with enough lead time to arrange financing, delay purchases, or accelerate collections.

Working Capital Levers

| Lever | How It Helps | Typical Impact |

|---|---|---|

| Supplier payment terms | Delay cash out by 30–60 days | High |

| Inventory turns optimization | Reduce dead stock tying up cash | Medium-High |

| Revenue-based financing | Advance against future sales | Medium |

| Pre-orders | Collect cash before purchasing inventory | High (if viable) |

| Marketplace payout acceleration | Some platforms offer early payouts | Low-Medium |

COGS and Margin Structure

Gross margin is the heartbeat of your e-commerce P&L. Many founders calculate it incorrectly by omitting costs that belong in COGS.

True COGS for E-commerce

Full COGS should include:

- Product cost (landed cost including import duties)

- Inbound shipping from supplier

- 3PL / warehouse storage and pick-and-pack fees

- Outbound shipping to customer

- Payment processing fees (typically 2–3%)

- Returns and restocking costs

- Packaging materials

When you include all of these, your gross margin will be 10–15 percentage points lower than what a naive calculation shows. This matters enormously for ecommerce financial planning — a business that thinks it has 50% gross margins but actually has 35% will run out of money building toward profitability targets that don’t exist.

Margin Benchmarks by Category

| Product Category | Typical Gross Margin |

|---|---|

| Fashion / Apparel | 45–65% |

| Beauty / Personal Care | 50–70% |

| Electronics | 10–25% |

| Home Goods | 30–50% |

| Food / Supplements | 40–60% |

| Sporting Goods | 30–50% |

If your gross margins fall significantly below category benchmarks, conduct a full cost reduction analysis before scaling further. Scaling poor margins only accelerates losses.

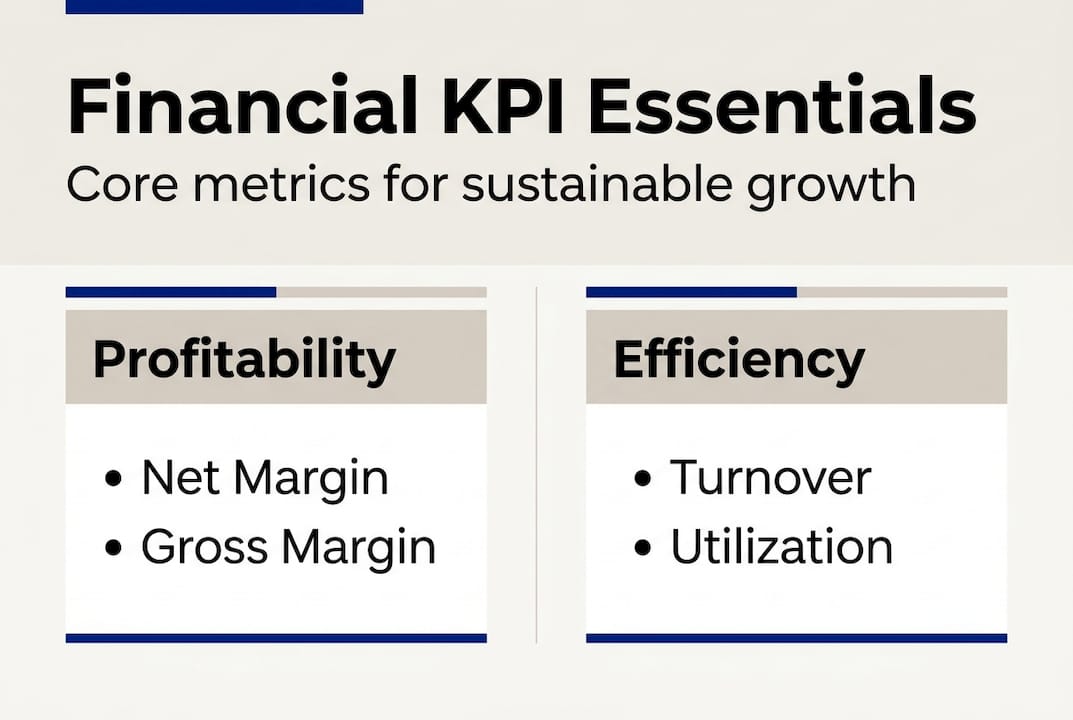

Essential Financial KPIs for E-commerce

Effective ecommerce financial planning requires tracking the right numbers consistently. Here are the metrics that actually drive decisions:

Revenue Quality Metrics

- Net Revenue (after returns and discounts) — never plan off gross revenue

- Average Order Value (AOV) — track weekly to catch product mix shifts

- Revenue per Customer — distinguishes transactional from loyal buyer bases

Profitability Metrics

- Gross Margin % — target above 40% for DTC brands

- Contribution Margin % — gross margin minus variable marketing costs

- EBITDA Margin — operating profitability before non-cash items

Growth Efficiency Metrics

- CAC Payback Period — months to recover customer acquisition cost

- ROAS (Return on Ad Spend) — revenue per dollar of ad spend

- MER (Marketing Efficiency Ratio) — total revenue ÷ total marketing spend

For a deeper dive into tracking these numbers, see our guide to mastering financial KPIs for business growth.

Inventory Metrics

- Inventory Turnover — how many times you sell through your inventory per year

- Days of Inventory On Hand (DOH) — inventory balance ÷ daily COGS

- Sell-Through Rate — units sold ÷ units available, critical for seasonal products

Budgeting and Forecasting for Seasonal Businesses

E-commerce forecasting is harder than most business forecasting because demand is inherently lumpy — tied to promotions, seasons, platform algorithm changes, and macroeconomic sentiment. A single viral post or Google algorithm update can swing monthly revenue by 30%.

Building a Three-Scenario Forecast

For every planning period, model three scenarios:

- Base case: Continuation of recent trends with modest seasonal adjustments

- Upside case: Successful new product launches, improved ROAS, faster customer acquisition

- Downside case: Ad cost spike, supplier delays, market softening

The downside case is not pessimism — it’s the scenario you need to survive. Your cash reserves, credit facilities, and operational flexibility should be sized to weather the downside case without existential threat to the business.

Seasonal Planning Framework

For businesses with strong Q4 seasonality (Black Friday, holiday), your annual planning should work backwards from peak season:

- Forecast Q4 revenue by category

- Calculate inventory requirements 60–90 days ahead (purchase by August–September)

- Determine cash needed for inventory purchase

- Model Q4 marketing spend and contribution margin

- Identify financing gap between cash available and cash needed

- Arrange financing in Q2–Q3, before peak season pressure hits

Understanding your break-even point for each season is essential — it tells you the minimum revenue needed to cover your seasonal fixed and variable cost commitments.

Scaling Profitably: When Growth Destroys Value

The most dangerous phase for an e-commerce business is rapid growth with underdeveloped financial systems. Here’s what typically goes wrong:

The Revenue Trap

A founder hits $1M in revenue and immediately reinvests everything into inventory and ads to hit $2M. At $2M, they reinvest again. At $3M, they realize they’ve never actually extracted profit from the business — and they’re now running a much larger, more complex operation on the same thin margins as when they started.

Profitable scaling requires setting explicit margin floors before growth investments. If your contribution margin falls below 20%, pause scaling and diagnose the cause before it compounds.

Case Study: The Margin Compression Spiral

An outdoor gear brand we worked with scaled from $800K to $2.4M in 18 months. Revenue tripled, but net profit went from $95K to $12K. The culprits:

- Ad costs increased 40% as they competed in more competitive keywords

- AOV dropped 15% as they added lower-margin product lines to drive volume

- Returns jumped from 8% to 14% as product quality control suffered under volume

- 3PL fees increased disproportionately as SKU count grew

Each of these was visible in the financial data — but no one was looking. A monthly review of core KPIs would have caught the compression early enough to course-correct.

How Fractional CFO Support Helps

Many e-commerce brands at $1M–$10M in revenue are too large to operate without financial oversight but too small to afford a full-time CFO. A fractional CFO brings institutional-grade ecommerce financial planning discipline — cash flow modeling, unit economics tracking, fundraising support — at a fraction of the cost.

E-commerce Financial Planning Checklist

- ☐ Calculate true COGS including all fulfillment, payment, and return costs

- ☐ Track gross margin monthly by product category

- ☐ Build a 13-week rolling cash flow forecast and review it weekly

- ☐ Calculate CAC and LTV by acquisition channel

- ☐ Set a minimum contribution margin floor before scaling ad spend

- ☐ Monitor inventory turnover and days-on-hand monthly

- ☐ Build 3-scenario annual forecast including downside case

- ☐ Model seasonal inventory cash requirements 90 days in advance

- ☐ Track return rate by product line and flag anything above 15%

- ☐ Review LTV:CAC ratio quarterly and set minimum acceptable threshold

- ☐ Set explicit profit extraction targets — don’t let growth consume all cash

Ready to Build a Profitable E-commerce Business?

Sound ecommerce financial planning is the difference between a business that grows and one that grows profitably. If you’re running an online store between $500K and $20M in revenue and want to build financial systems that actually support your growth, we can help.

Book a free consultation with John Galt Finance and get a clear picture of your e-commerce unit economics, cash position, and path to sustainable profit.

FAQ

What is ecommerce financial planning?

Ecommerce financial planning is the process of building financial models, forecasts, and KPI frameworks specifically designed for online retail businesses. It covers unit economics (CAC, LTV, contribution margin), cash flow management (especially the inventory funding gap), P&L structuring, and seasonal forecasting — all calibrated to the unique dynamics of e-commerce operations.

What gross margin should an e-commerce business target?

Most DTC (direct-to-consumer) e-commerce brands should target gross margins of 40–60% after including all true variable costs: product cost, inbound shipping, fulfillment, outbound shipping, payment processing, and returns. Businesses below 30% gross margin typically struggle to achieve profitability because there isn’t enough margin to cover marketing, overhead, and growth investment.

How much cash reserve does an e-commerce business need?

A minimum of 8–12 weeks of operating expenses as cash reserve is a reasonable baseline. However, for seasonal businesses, you need to model the peak inventory purchase requirement separately and ensure you have access to that capital — either from reserves or a credit facility — before the buying season begins.

When does an e-commerce business need a CFO?

Most e-commerce businesses benefit from fractional CFO support once they cross $1M in annual revenue. At this stage, financial complexity — multiple SKUs, ad channels, supplier relationships, inventory management — exceeds what a bookkeeper or basic accounting software can effectively manage. A fractional CFO provides cash flow modeling, unit economics tracking, and fundraising support without a full-time salary commitment.

How should e-commerce businesses forecast for Black Friday?

Start your Black Friday forecast in Q2. Model expected revenue by product line, calculate inventory requirements 90 days in advance, determine the cash needed to fund those purchases, and identify your financing gap. Most founders who run into cash problems during peak season waited too long — they modeled revenue in August and realized they needed inventory cash in September, leaving almost no time to arrange financing.