Most SMB owners are running their finances on delayed information, outdated spreadsheets, and a vague sense of where the money went. Financial reporting best practices exist precisely to fix that gap. When your reports are accurate, timely, and structured the way a CFO would build them, they stop being a compliance obligation and start being the clearest tool you have for making confident decisions. This article covers what your reporting framework should include, which practices actually move the needle, and where most owners quietly go wrong.

Table of Contents

- Establishing core financial reporting criteria for SMB success

- Key financial reporting best practices for SMBs

- Leveraging technology and internal controls to improve reporting accuracy

- Aligning with IFRS for SMEs standards to simplify financial reporting

- Comparing common financial reporting practices: what works best for SMBs

- The overlooked truth most SMBs miss about financial reporting best practices

- Unlock growth with expert CFO-led financial reporting solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Core financial statements | SMBs should prepare income, balance sheet, equity, and cash flow statements monthly for clear financial insight. |

| Rolling forecasts matter | Weekly updated 13-week cash flow forecasts help SMBs manage liquidity and avoid failure. |

| Automate and control | Integrate technology and internal controls to cut errors and speed reporting cycles. |

| Align with IFRS | Using IFRS for SMEs simplifies reporting and enhances transparency while reducing costs. |

| Cash reserves save businesses | Maintaining 3-6 months of cash reserves prevents over 80% of cash flow crises in SMBs. |

Establishing core financial reporting criteria for SMB success

Before you can improve your reporting, you need to define what good reporting actually looks like for a business your size. The answer is more specific than most people expect.

Small businesses should prepare four core financial statements monthly: the income statement, balance sheet, shareholders’ equity statement, and cash flow statement. Not quarterly. Not at year-end. Monthly. Each of these documents answers a different question. The income statement tells you whether the business is profitable. The balance sheet shows what you own versus what you owe. The shareholders’ equity statement tracks ownership value over time. The cash flow statement, often the most important for SMBs, reveals whether your business actually has money to operate, regardless of what the income statement says.

Frequency matters as much as content. SMB financial statements reviewed monthly, quarterly, and annually with deliberate time allocations create the kind of layered visibility that drives operational efficiency. Monthly reviews keep you current on income and cash. Quarterly reviews of the balance sheet catch structural issues before they compound. Annual reviews give you the trend data to make credible growth plans.

Compliance is the third leg of the stool. For SMBs operating globally or seeking investor backing, aligning with IFRS for SMEs accounting standards reduces the burden of full IFRS compliance while still producing reports that stakeholders trust. This is not just a legal checkbox. Reporting that meets recognized standards signals financial discipline to lenders, acquirers, and partners.

Here is what your core reporting criteria should cover:

- Four financial statements prepared and reviewed monthly

- Quarterly balance sheet analysis to track asset and liability shifts

- Annual trend review comparing at least two to three years of data

- Compliance with IFRS for SMEs or a regionally recognized equivalent

- Stakeholder-ready formatting that any investor or lender can read without a guide

Strong financial analysis for SMBs starts at this foundation. Without it, everything downstream, including forecasting, budgeting, and fundraising, is built on sand. The essential financial metrics for SMBs you track are only as reliable as the reports feeding them.

Key financial reporting best practices for SMBs

Having established foundational criteria, let’s look at the specific practices that drive financial reporting excellence.

82% of small business failures stem from cash flow mismanagement. That number should stop you cold. It means the majority of businesses that fail are not failing because of a bad product or a saturated market. They run out of cash because no one was watching the right numbers at the right time.

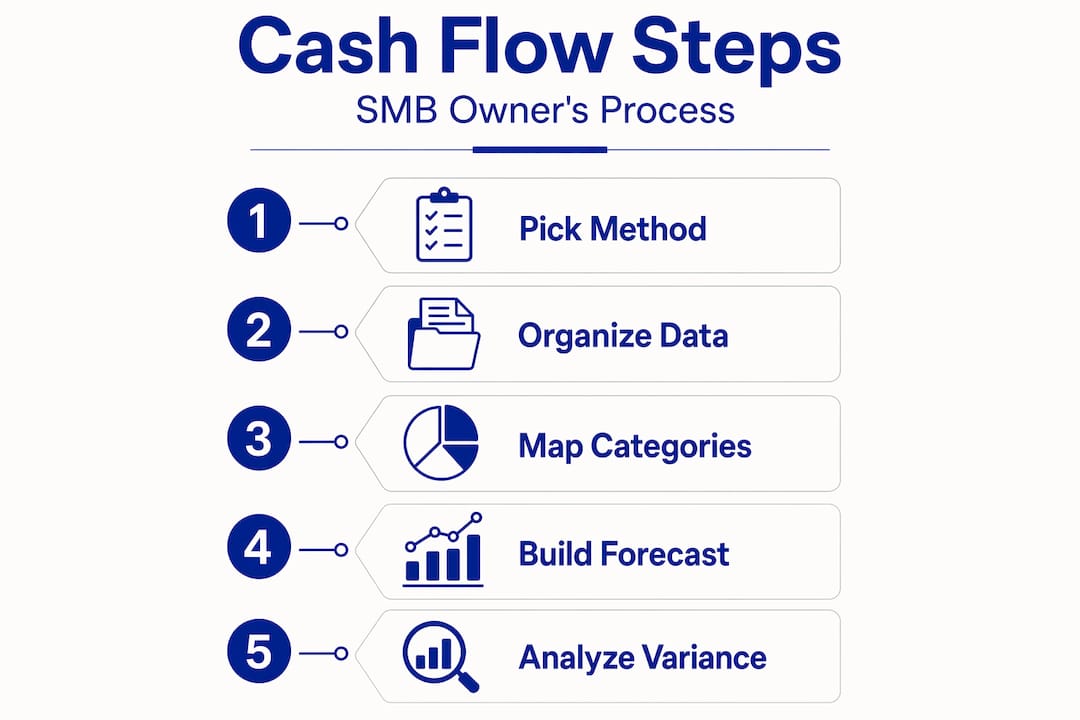

The CFO-level response to that risk is the 13-week rolling cash flow forecast, updated every week. This is not a projection you build once and revisit in December. It is a living document that shows you exactly what cash you expect to receive and spend across the next quarter, updated as reality changes. Pair it with good cash flow management strategies and you are no longer guessing.

Here are the core practices to build into your reporting system:

- Run a 13-week rolling cash flow forecast. Update it weekly. Flag any week where projected outflows exceed inflows so you can act before the gap opens, not after.

- Separate your operating and tax accounts. When tax obligations sit in the same account as operating funds, it is too easy to spend money you do not actually have. Segregation removes the temptation and the confusion.

- Keep 3 to 6 months of operating expenses in cash reserves. This is the buffer that keeps a slow month from becoming a crisis. Most SMBs underestimate this figure by half.

- Shorten payment terms and incentivize early payment. Net-30 or net-60 terms transfer your cash to your customers for weeks. A 2% discount for payment within 10 days often costs less than a short-term credit line.

- Reconcile accounts weekly or monthly without exception. Errors caught within days are correctable. Errors discovered at year-end become audit problems.

Pro Tip: If your team reconciles once a month and consistently finds discrepancies over $1,000, move to weekly reconciliation immediately. The time cost is far lower than the cleanup cost.

This is also where a solid cash flow forecasting guide becomes a practical tool, not just theory. The discipline of weekly updates forces your team to stay close to real numbers rather than comfortable projections.

Leveraging technology and internal controls to improve reporting accuracy

Technology and controls enhance accuracy, but understanding reporting standards guides proper presentation next.

SMBs waste 4 to 6 weeks on monthly closes using spreadsheets. The same report notes that integrating ERP and CRM systems via APIs flags 90% of anomalies through AI before any manual review happens. That is not a small efficiency gain. It is the difference between a finance function that enables decisions and one that just documents what already happened.

Automation of the monthly close is now accessible to businesses well below the enterprise level. Cloud-based accounting platforms connect directly to your bank, your invoicing system, and your payroll provider. When those feeds are live, your close shifts from a two-week reconciliation exercise to a one-to-two-day review and sign-off.

Here is what a technology-supported reporting setup looks like in practice:

- ERP and CRM integration that syncs transaction data automatically, reducing manual entry errors

- AI-powered anomaly detection that flags unusual entries, duplicate payments, or out-of-pattern expenses before they reach the report

- Real-time dashboards that let you see margin trends, cash position, and receivables aging without opening a spreadsheet

- Automated alerts tied to threshold rules, for example, when a cost category exceeds budget by more than 10%

Internal controls are not just an audit requirement. They are the architecture that makes your financial data trustworthy enough to act on.

Internal controls like segregation of duties prevent 70% of financial errors in SMBs and materially increase stakeholder trust. In practice, this means one person handles revenue recognition, a different person approves payments, and a third person performs reconciliations. No single employee controls an entire transaction cycle.

Pro Tip: You do not need a large team to implement segregation of duties. In a small finance function, the business owner can serve as the approver while a bookkeeper handles processing. The key is that no single person can both initiate and approve a transaction.

The payoff for investing in these controls shows up in creating impactful financial reports that leadership, investors, and lenders can trust without reservations. If you want to apply strategic finance best practices at a level that scales with your business, internal controls are where you start.

Aligning with IFRS for SMEs standards to simplify financial reporting

Having explored standards alignment, let’s compare best practice elements side-by-side for decision clarity.

The IFRS for SMEs third edition updates Section 19 on Business Combinations, aligning it with IFRS 3 while simplifying the reporting requirements for SMEs, effective 2026. This matters because many SMBs operating internationally have struggled with the gap between full IFRS, designed for large public companies, and simplified local standards that do not always satisfy foreign investors or lenders.

The updated standard reduces reporting complexity without sacrificing the transparency that stakeholders require. Revenue recognition rules are clearer. Business combination accounting is more straightforward. And the IASB has added educational modules that reduce preparation time by 40% while improving compliance and comprehension.

Here is a comparison of key changes between the second and third editions:

| Area | Second edition | Third edition (2026) |

|---|---|---|

| Business combinations (Section 19) | Diverged from full IFRS 3 | Aligned with updated IFRS 3 |

| Revenue recognition | Simplified but inconsistent with IFRS 15 | Closer alignment with IFRS 15 principles |

| Educational support | Limited guidance materials | New modules cutting prep time by 40% |

| Effective date | Ongoing | Effective for periods beginning 2026 |

| Stakeholder transparency | Moderate | Enhanced through updated disclosures |

For SMBs eyeing cross-border transactions, a funding round, or a future exit, aligning early with latest IFRS for SMEs updates is an investment that pays off in due diligence. Buyers and investors do not want to restate your financials. The more your reports already conform to a recognized standard, the cleaner your numbers look under scrutiny.

Comparing common financial reporting practices: what works best for SMBs

With detailed comparison complete, we turn to expert perspective on elevating SMB reporting further.

Not every reporting approach delivers equal results. The table below draws on monthly, quarterly, and annual review frameworks recommended for SMBs, alongside technology and control variables.

| Practice | Benefit | Drawback | Best fit |

|---|---|---|---|

| Monthly financial reviews | Catches issues early, keeps data current | Requires dedicated time and process | All SMBs with active operations |

| Quarterly reviews only | Lower time commitment | Too infrequent to catch cash problems | Very early-stage businesses only |

| Annual-only review | Minimal ongoing effort | High risk of costly surprises | Not recommended for any SMB |

| Manual spreadsheet close | Low upfront cost | 4 to 6 weeks of lost time monthly | No SMB with growth ambitions |

| ERP/AI-integrated close | Flags 90% of anomalies automatically | Initial setup investment | SMBs with revenue above $500K |

| Static annual budget | Easy to build once | Irrelevant within weeks of real operations | Not recommended without monthly updates |

| Rolling 13-week forecast | Reflects real cash position weekly | Requires discipline to update | All SMBs with payroll or variable costs |

| No internal controls | Fast and simple initially | Prevents 70% more errors when applied | No SMB should skip controls |

The pattern is clear. Frequency, automation, and controls consistently outperform the lower-effort alternatives, not in theory but in the error rates, close times, and cash outcomes they produce. The financial analysis techniques that generate real insight require data you can trust. That trust is built through the practices in the left column, not shortcuts.

The overlooked truth most SMBs miss about financial reporting best practices

Here is what most articles about financial reporting will not tell you: the problem is rarely technical. SMB owners know they should review their financials regularly. They know cash flow matters. They know automation exists. The real issue is that reporting gets treated as a backward-looking record of what happened, when its actual value is forward-looking.

A CFO does not read last month’s income statement to confirm what they already know. They read it to identify what changes next. When gross margin drops two points, the question is not “why did that happen?” It is “which product line, which customer segment, and which operational decision caused it, and what do we change this week?”

Maintaining 3 to 6 months of operating expenses in cash reserves is one of the most cited best practices in SMB finance and one of the most ignored. Owners build the reserve, then raid it to fund a growth initiative before the reporting system can flag that the move compromises solvency. Static annual budgets make this worse. They create a false sense of plan adherence while the actual cash position drifts toward danger.

Rolling forecasts work because they force a confrontation with reality every single week. You cannot hide behind a budget that was set in October when your rolling forecast shows you running out of runway in six weeks.

The other gap we see consistently is internal controls treated as audit preparation rather than daily operating infrastructure. Controls are not for your accountant. They are for you. They are the mechanism that ensures the numbers you are reading actually reflect what happened in your business, not what someone recorded out of convenience.

The SMBs that grow with confidence are not the ones with the most sophisticated tools. They are the ones that read their financials with enough discipline to act on what they see. A fractional CFO can install that discipline without the full-time cost, but the mindset shift has to come from the owner first.

Unlock growth with expert CFO-led financial reporting solutions

Knowing the best practices is one thing. Having a system that delivers them consistently, every month, without requiring you to become a financial expert, is another. That is where John Galt Finance works alongside SMB owners.

Our CFO-led financial analysis services translate raw reporting data into decisions your business can act on this week. We build rolling forecasts, design internal controls scaled to your team size, and close your books faster using integrated financial models tailored to your industry. The custom financial modeling process we use is built around your revenue structure, cost profile, and growth targets, not a generic template. And our cash flow forecasting solutions give you the 13-week visibility that separates businesses that scale from ones that stall.

Frequently asked questions

What are the essential financial statements SMBs should prepare monthly?

SMBs should prepare four statements monthly: the income statement, balance sheet, shareholders’ equity statement, and cash flow statement to maintain accurate financial visibility and compliance readiness.

Why is a 13-week rolling cash flow forecast critical for SMBs?

Because 82% of small business failures trace back to cash flow problems, a 13-week rolling forecast updated weekly gives SMBs the lead time to act before a liquidity gap becomes a crisis.

How do internal controls improve SMB financial reporting?

Segregation of duties prevents 70% of financial errors in SMBs, increases stakeholder trust, and ensures report accuracy beyond what basic compliance alone requires.

What benefits does aligning with IFRS for SMEs provide SMBs?

IFRS for SMEs third edition simplifies compliance by aligning with full IFRS, and updated educational resources reduce preparation effort by up to 40% while improving transparency for investors and lenders.

What are common financial reporting mistakes SMBs make?

The most damaging common financial planning mistakes include reviewing financials only annually, ignoring real cash flow data, using overly optimistic projections, and never stress-testing scenarios against a downturn.