Remote CFO Service Benchmarks

| Metric | Benchmark |

|---|---|

| Cost savings vs on-site full-time CFO | 60-75% |

| Remote CFO retainer (SMB) | $3,000-$10,000/month |

| Time zone overlap with US client (best practice) | 4+ hours daily |

| Cadence of video sync with CEO | Weekly (60-90 min) |

| Standard tooling | QuickBooks/Xero, G-Suite, Slack, Loom, Excel/Google Sheets |

| Onboarding time (remote) | 30-45 days |

| Adoption of remote CFO since 2020 | +300% (CFO.com industry survey) |

| Net Promoter Score (top remote CFO firms) | >60 |

Most small and medium business owners assume that a CFO is a luxury reserved for large corporations with deep pockets and sprawling finance departments. That assumption is costing businesses real money. Remote CFO services shatter that barrier by delivering high-level financial strategy, forecasting, and performance insight on a flexible, scalable basis. Whether you’re running a $1 million service business or a $15 million manufacturing operation, strategic financial guidance is not out of reach. This article breaks down exactly what remote CFO services include, how they compare to traditional options, and how to get started in a way that makes sense for your business.

Table of Contents

- Understanding remote CFO services

- Remote vs. traditional CFO: Key differences for business owners

- Strategic benefits of remote CFO services for SMBs

- How to choose and get started with a remote CFO

- Why most SMBs underestimate remote CFO impact

- Get started: Unlock SMB growth with remote CFO solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Strategic expertise | Remote CFOs provide unbiased strategic financial guidance for SMB growth. |

| Flexible solutions | Outsourced CFO services help optimize operations without fixed costs. |

| Industry benchmarking | Remote CFOs use industry benchmarks to drive performance improvement. |

| Easy onboarding | Selecting the right remote CFO can be streamlined with clear criteria. |

Understanding remote CFO services

Remote CFO services give your business access to a senior financial strategist without the cost or commitment of a full-time hire. Instead of sitting in your office, a remote CFO works virtually, often on a fractional or contract basis, meaning you pay for the expertise you need without funding a six-figure salary, benefits package, and office overhead.

The scope of work goes well beyond bookkeeping or tax preparation. A remote CFO focuses on the strategic layer of your finances. That includes building financial models, running scenario analysis (testing what happens to your cash if revenue drops 20%, for example), managing cash flow cycles, setting performance benchmarks, and advising on growth decisions like new product launches, acquisitions, or fundraising rounds.

Here’s what a typical remote CFO engagement covers:

- Financial planning and budgeting: Building annual plans and rolling forecasts tied to your business goals

- Cash flow management: Identifying cash gaps before they become crises and structuring payment cycles to improve liquidity

- Scenario and sensitivity analysis: Modeling best-case, base-case, and worst-case outcomes so you can make confident decisions

- Performance benchmarking: Comparing your margins, costs, and revenue metrics against industry standards

- Strategic guidance: Advising on pricing, growth investments, cost structure, and capital allocation

- Fundraising support: Preparing investor-ready financial models and narratives for lenders or equity investors

According to an outsourced CFO services guide, remote CFOs focus on strategic finance, keep industry benchmarks, and deliver unbiased guidance, which is something an internal hire embedded in daily operations often struggles to do objectively.

The delivery model matters too. Most remote CFO engagements use cloud-based tools such as QuickBooks, Xero, or specialized financial modeling platforms. You share access to your financial data, and the CFO builds, updates, and presents reports on a regular cadence, monthly, quarterly, or whatever your business needs.

Pro Tip: Before shortlisting any remote CFO, ask which accounting software and financial modeling tools they use. Compatibility with your existing systems will save hours of setup time and reduce the risk of data errors from the very start.

For SMB owners who want a deeper breakdown of how this model works in practice, a fractional CFO guide covers the engagement structure from first contact to ongoing support.

Remote vs. traditional CFO: Key differences for business owners

Understanding the structure of remote CFO services is step one. The more useful question for most business owners is: how does this actually compare to hiring someone full-time?

Here’s a direct comparison across the factors that matter most:

| Factor | Remote CFO | Traditional in-house CFO |

|---|---|---|

| Cost | $2,000 to $10,000/month | $180,000 to $300,000+/year |

| Availability | Scheduled, project-based | Full-time, on-site |

| Industry perspective | Broad, cross-industry insight | Narrow, company-specific |

| Strategic focus | High | Mixed with operational tasks |

| Integration depth | Moderate | Deep |

| Flexibility | High, scalable up or down | Low, fixed commitment |

| Onboarding time | Days to weeks | Months |

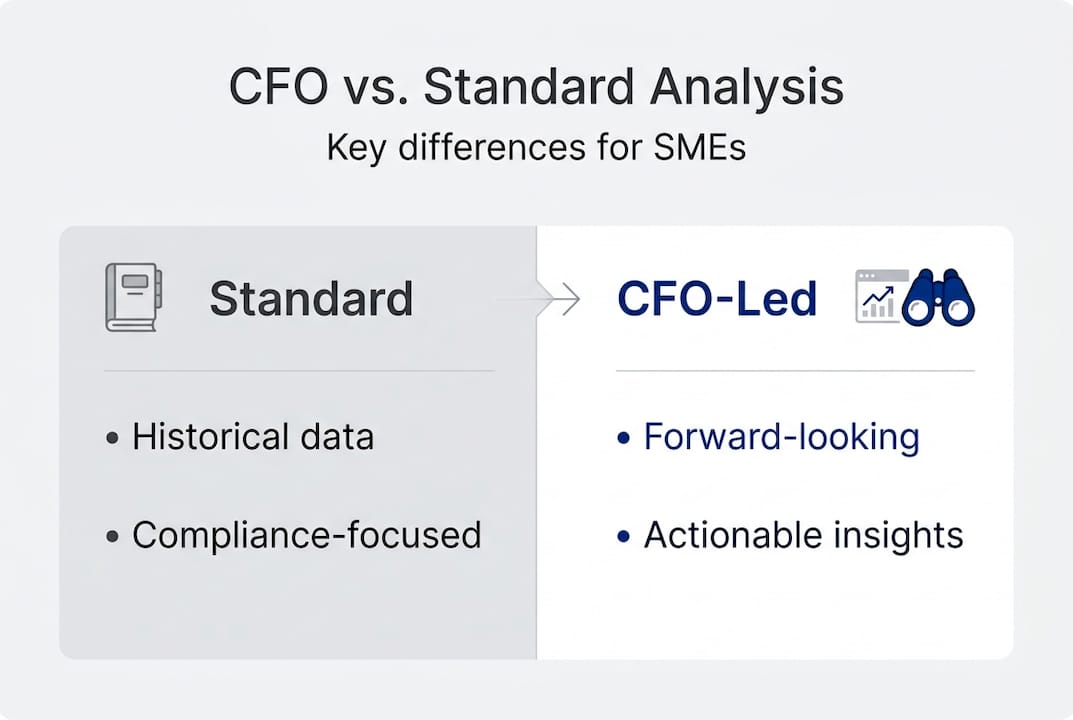

The strategic focus column deserves particular attention. A traditional CFO often gets pulled into operational fire-fighting: signing checks, managing the accounting team, handling compliance deadlines. A remote CFO, by contrast, stays at the strategic level by design.

“Fractional CFOs bring unbiased views and industry benchmarks but are less embedded in the day-to-day.” That distance is actually an asset. It means the advice you get is grounded in what works across multiple businesses, not just what feels comfortable inside yours.

Advantages of a remote CFO:

- Lower cost with immediate access to senior expertise

- Fresh perspective unclouded by internal politics

- Broad benchmarking from working across multiple industries

- Scales as your business grows or contracts

- Faster to engage than a full recruitment process

Disadvantages of a remote CFO:

- Less day-to-day operational involvement

- May require stronger internal bookkeeping support

- Relationship building takes intentional effort in a virtual setup

Advantages of a traditional in-house CFO:

- Deep integration with your team and operations

- Available for real-time decisions and daily financial oversight

- Stronger relationship with lenders, auditors, and internal staff

Disadvantages of a traditional in-house CFO:

- High fixed cost regardless of business performance

- Can develop blind spots from being too close to the business

- Slower to hire and expensive to replace

Understanding these finance leadership differences helps you match the right model to your business stage. Most SMBs earning between $500K and $10 million will get far more strategic value per dollar from a remote CFO than from a full-time hire. And knowing specifically what fractional CFO duties look like in practice makes it easier to set clear expectations before signing anything.

Strategic benefits of remote CFO services for SMBs

Comparing options is useful, but what really matters is what a remote CFO actually does for your bottom line. The benefits are concrete, measurable, and often underestimated by business owners who have never worked with a CFO-level advisor before.

Remote CFOs focus on strategic improvement rather than day-to-day operations, and that focus translates into real business outcomes. Here are the most common strategic deliverables and what they deliver:

| Deliverable | What it solves | Business impact |

|---|---|---|

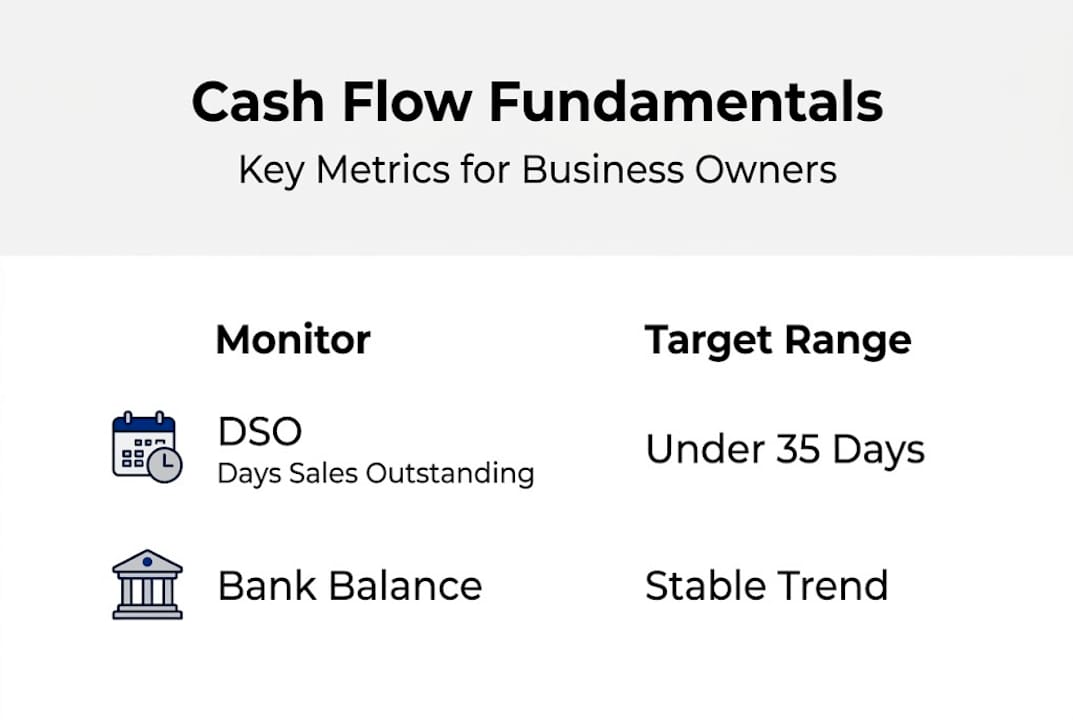

| 13-week cash flow forecast | Cash shortfalls and surprise gaps | Avoids emergency borrowing |

| Financial model with scenarios | Uncertainty in growth planning | Confident investment decisions |

| Profitability analysis by product/service | Hidden loss-making revenue streams | Margin improvement |

| Industry benchmarking report | Unknown performance gaps | Competitive cost structure |

| Fundraising-ready financial package | Investor skepticism | Faster, better-term capital |

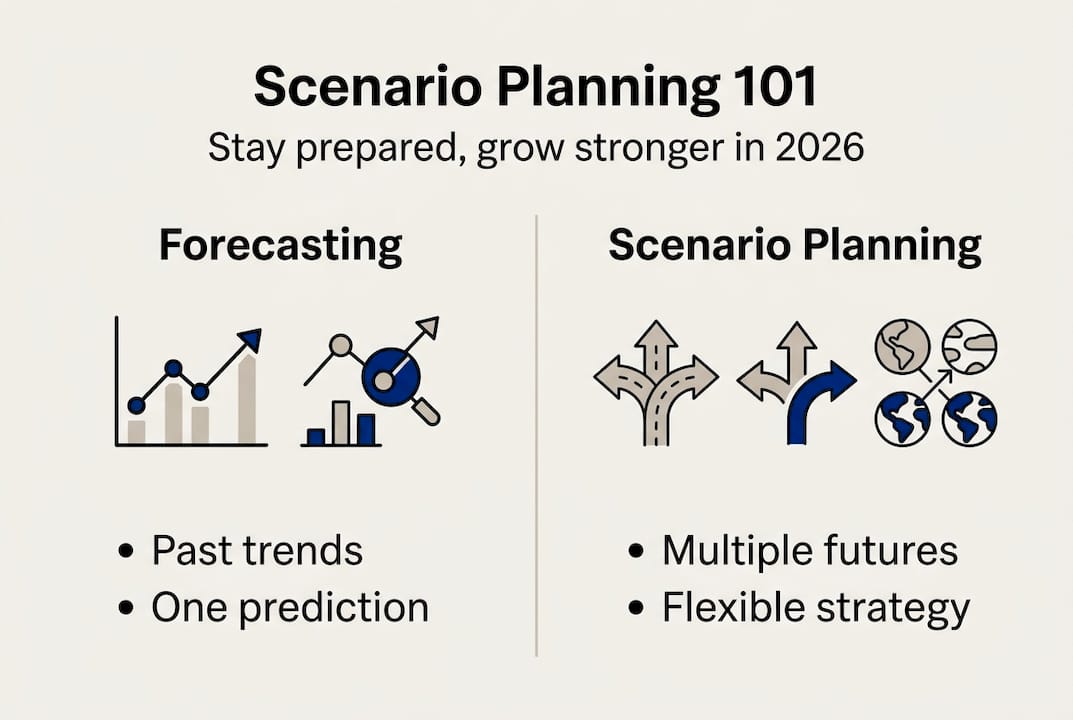

Scenario planning is one of the most powerful tools in a remote CFO’s kit. When you’re deciding whether to hire two more sales reps, open a second location, or take on a large contract, the risk feels intuitive but the numbers are fuzzy. A remote CFO builds the model that shows you what your cash looks like under each decision, so you stop guessing and start choosing with evidence.

Here’s how to integrate a remote CFO into your business effectively:

- Audit your current financial data quality. Clean, accurate books are the foundation. Before your CFO can forecast, they need reliable historical data.

- Define your top three financial priorities. Growth funding? Cash flow stability? Margin improvement? A focused mandate drives faster results.

- Establish a reporting cadence. Agree on when and how you’ll meet, what reports will be delivered, and who owns the numbers internally.

- Assign an internal point of contact. This is usually your bookkeeper or office manager. They’ll handle data requests and keep the workflow moving.

- Review progress monthly. Set a monthly check-in to review actuals versus forecast, discuss variances, and adjust strategy accordingly.

This process sounds simple, but most SMBs skip step one and two, which leads to wasted time and frustration on both sides. A remote CFO is not a miracle worker. They need accurate inputs and a clear mandate to deliver results.

For business owners wondering whether the timing is right, a guide on when to hire a CFO outlines the specific financial signals that suggest you’re ready. And if you want broader context on how CFO services fit into SMB growth strategy, the SME CFO services guide covers the full picture.

Pro Tip: Before signing any remote CFO contract, document your top three deliverables in writing. This gives both sides clear accountability and makes it easy to measure whether the engagement is delivering value after 90 days.

How to choose and get started with a remote CFO

With the benefits clear, the next step is finding the right partner. The market for remote CFO services has grown significantly, and not every provider offers the same depth of expertise. Selection should be based on industry experience, tech stack, and deliverables, not just price or availability.

Here’s a step-by-step process for evaluating and engaging a remote CFO:

- Define your scope before you start searching. Do you need ongoing monthly support, a one-time financial model, or help preparing for a fundraise? Knowing this narrows your search considerably.

- Build a shortlist based on industry experience. A CFO who has worked with SaaS companies will understand your metrics. One who specializes in manufacturing understands your cost structure. Match their background to your business model.

- Evaluate their technology. Ask specifically which tools they use for modeling, reporting, and communication. They should be fluent in at least one major accounting platform and a modeling tool like Excel, Google Sheets, or dedicated FP&A (financial planning and analysis) software.

- Request a sample deliverable. Ask to see an anonymized financial model or report they’ve produced for a similar client. This tells you more than any sales conversation.

- Run a paid pilot project. Before committing to a long-term contract, engage the CFO for a defined project such as a cash flow forecast or a profitability review. You’ll learn quickly whether the working relationship fits.

- Negotiate a clear contract. Define deliverables, response times, reporting formats, and exit terms upfront. Ambiguity in the contract leads to frustration later.

Before you hire, ask these essential questions:

- What industries have you served, and do you have clients similar to mine?

- What does your typical monthly engagement look like in terms of hours and deliverables?

- How do you handle urgent financial questions outside of scheduled calls?

- Can you provide references from clients at a similar revenue stage?

- How do you stay current on industry benchmarks and regulatory changes relevant to my business?

Good strategic finance practices start with choosing the right partner, not just the cheapest one. Many SMBs make the mistake of comparing remote CFO fees to bookkeeping rates. That’s the wrong benchmark. The right comparison is the value of the decisions a CFO enables versus the cost of making those decisions without good data.

It’s also worth understanding where a remote CFO fits in relation to your existing financial support. If you’re unsure about the division of responsibilities, reading about the difference between a bookkeeper and CFO can clarify who does what and ensure your team structure actually supports strategic growth rather than just compliance.

Why most SMBs underestimate remote CFO impact

Here’s an uncomfortable truth: most SMB owners who hesitate on remote CFO services aren’t actually worried about cost. They’re worried it won’t work for a business their size. That belief is wrong, and it’s one of the most expensive assumptions a growing business can make.

The businesses that benefit most from remote CFO services are not the ones with complex org charts or investor boards. They’re the ones making major decisions, like taking on debt, hiring aggressively, or launching a new product line, without a single financial model to guide them. That’s where the risk lives. And that’s exactly where a remote CFO adds the most value.

Remote CFOs bring perspective that internal teams simply cannot generate on their own. They’ve seen how similar businesses handled similar crossroads. They carry benchmarks from across industries. They read the warning signs in your cash flow that you’re too close to the business to notice. These CFO need signals often appear long before a crisis hits, but only someone trained to read them can act in time.

The real missed opportunity isn’t paying for a remote CFO. It’s the cost of every strategic decision made without one: the pricing model that quietly erodes your margins, the growth investment that misses its targets, or the cash crunch that forces a rushed loan at unfavorable terms. Strategic finance is not a luxury. For any SMB serious about growth, it’s the foundation everything else is built on.

Get started: Unlock SMB growth with remote CFO solutions

If this article has clarified what remote CFO services can do for your business, the next move is simple: explore what a tailored engagement looks like for your specific situation.

At John Galt Finance, we work with SMBs across diverse industries to deliver outsourced CFO-level expertise without the full-time price tag. Our services include financial modeling for growth tailored to your business model, a cash flow forecasting guide to help you anticipate and manage liquidity, and strategic financial planning that positions your company for sustainable expansion. Whether you’re preparing for a fundraise, optimizing margins, or simply trying to understand where your money goes, our fractional CFO solutions are built to move fast and deliver results that actually show up in your financials.

Frequently asked questions

What does a remote CFO service include?

Remote CFO services typically cover financial planning, budgeting, cash flow management, and strategic guidance delivered virtually, including services like strategic finance and benchmarking tailored to your business stage and industry.

Is a remote CFO as effective as an in-house CFO?

Remote CFOs offer strong strategic expertise and unbiased perspectives, though as fractional CFOs focus on strategic work rather than daily operations, they are less involved in routine financial management than a full-time internal hire.

How do I choose the right remote CFO?

Look for industry-specific experience, technology compatibility, and clearly defined deliverables, since selection based on industry experience and deliverables is the most reliable predictor of a successful engagement.

Can remote CFOs help with cash flow and growth planning?

Yes. Remote CFOs specialize in scenario analysis and forecasting models that help SMBs plan for growth, manage risk, and maintain healthy liquidity across different business conditions.

Recommended

- Why SMEs Need CFO Services: Unlock Growth and Clarity

- Essential financial metrics to track for SMB growth: 2026

- Unlock business growth with a custom financial modeling process

- Cash flow management: 60% of SMBs struggle in 2026

FAQ

Can a remote CFO be as effective as on-site?

Yes for 95% of CFO work, which is analytical (modeling, forecasting, board prep). On-site adds value for team management, deal negotiation, and culture work. Most SMBs are better served by a senior remote CFO than a junior on-site one at the same cost.

What tools make remote CFO work effective?

Standard stack: cloud accounting (QuickBooks Online or Xero), shared docs (Google Workspace), messaging (Slack), async video (Loom), forecasting (Excel or a tool like Jirav/Fathom). The bottleneck is rarely tools; it’s data hygiene in the accounting system.

How do I evaluate a remote CFO?

Three checks: (1) sample deliverables (board pack, cash forecast), (2) reference calls with 2-3 current clients your size, (3) trial 30-day diagnostic engagement before signing 12 months. Avoid anyone who can’t show specific work product from comparable companies.

What time zones work for US SMBs?

4+ hours of overlap with your business day is the practical minimum. Eastern Europe and Latin America are the most common offshore CFO talent pools. Asia-based providers require either night work or strict async discipline; this usually trades cost for slower iteration.

How does a remote CFO integrate with my existing bookkeeper?

The bookkeeper owns transactional accuracy (close, reconciliations, AR/AP). The remote CFO owns forecasting, reporting, and strategy. Define handoffs in writing: bookkeeper closes by business day 7, CFO delivers variance and forecast by business day 10. See our outsourced finance team guide for org design.